How Does The Timing And The Size Of Cash Flows Affect The Payback Method

Upper-case letter Budgeting Decisions

64 Evaluate the Payback and Accounting Rate of Render in Capital Investment Decisions

Many companies are presented with investment opportunities continuously and must sift through both feasible and nonviable options to identify the best possible expenditure for business organization growth. The process to select the best option requires careful budgeting and analysis. In conducting their analysis, a company may utilize various evaluation methods with differing inputs and assay features. These methods are often broken into two broad categories: (1) those that consider the time value of money, or the fact that a dollar today differs from a dollar in the hereafter due to inflation and the power to invest today's money for future growth, and (2) those analysis methods that do not consider the time value of coin. We will examine the non-time value methods get-go.

Non-Fourth dimension Value Methods

Non-time value methods practise not compare the value of a dollar today to the value of a dollar in the time to come and are often used equally screening tools. Two not-time value evaluative methods are the payback method and the accounting rate of render.

Fundamentals of the Payback Method

The payback method (PM) computes the length of time it takes a company to recover their initial investment. In other words, it calculates how long it will take until either the amount earned or the costs saved are equal to or greater than the costs of the project. This tin exist useful when a company is focused solely on retrieving their funds from a project investment as quickly as possible.

Businesses do not want their money tied up in majuscule assets that have limited liquidity. The longer money is unavailable, the less power the company has to utilize these funds for other growth purposes. This extended length of fourth dimension is too a concern considering it produces a riskier opportunity. Therefore, a company would similar to get their money returned to them equally chop-chop as possible. One style to focus on this is to consider the payback period when making a capital budget conclusion. The payback method is express in that information technology simply considers the fourth dimension frame to recoup an investment based on expected almanac cash flows, and it doesn't consider the effects of the time value of coin.

The payback period is calculated when in that location are even or uneven annual cash flows. Greenbacks catamenia is money coming into or out of the company every bit a result of a concern action. A greenbacks inflow can be money received or price savings from a capital investment. A cash outflow tin can be money paid or increased toll expenditures from capital investment. Cash period volition estimate the ability of the visitor to pay long-term debt, its liquidity, and its power to grow. Cash flows appear on the statement of cash flows. Cash flows are different than net income. Cyberspace income will correspond all company activities affecting revenues and expenses regardless of the occurrence of a cash transaction and volition appear on the income statement.

A visitor will estimate the future cash inflows and outflows to be generated past the capital investment. Information technology's important to remember that the cash inflows can be caused by an increment in greenbacks receipts or by a reduction in cash expenditures. For example, if a new piece of equipment would reduce the production costs for a visitor from ?120,000 a year to ?lxxx,000 a year, we would consider this is a ?twoscore,000 cash arrival. While the company does not actually receive the ?xl,000 in cash, it does save ?40,000 in operating costs giving it a positive cash arrival of ?xl,000.

Cash flow tin also be generated through increased production volume. For example, a visitor purchases a new building costing ?100,000 that will allow them to business firm more space for product. This new space allows them to produce more production to sell, which increases cash sales by ?300,000. The ?300,000 is a new cash inflow.

The difference between greenbacks inflows and cash outflows is the net cash arrival or outflow, depending on which cash flow is larger.

Annual net greenbacks flows are and so related to the initial investment to determine a payback period in years. When the expected net annual cash flow is an even amount each period, payback tin be computed every bit follows:

The result is the number of years it will take to recover the cash made in the original investment. For example, a press company is considering a printer with an initial investment cost of ?150,000. They expect an annual cyberspace cash menstruation of ?20,000. The payback period is

\(\text{Payback Menses}=\frac{?150,000}{?twenty,000}=vii.5\phantom{\dominion{0.2em}{0ex}}\text{years}\)

The initial investment toll of ?150,000 is divided by the annual greenbacks period of ?20,000 to compute an expected payback period of 7.5 years. Depending on the visitor's payback period requirements for this type of investment, they may laissez passer this option through the screening process to be considered in a preference decision. For example, the company might require a payback menstruation of 5 years. Since 7.5 years is greater than 5 years, the visitor would probably not consider moving this alternative to a preference decision. If the company required a payback period of 9 years, the company would consider moving this alternative to a preference conclusion, since the number of years is less than the requirement.

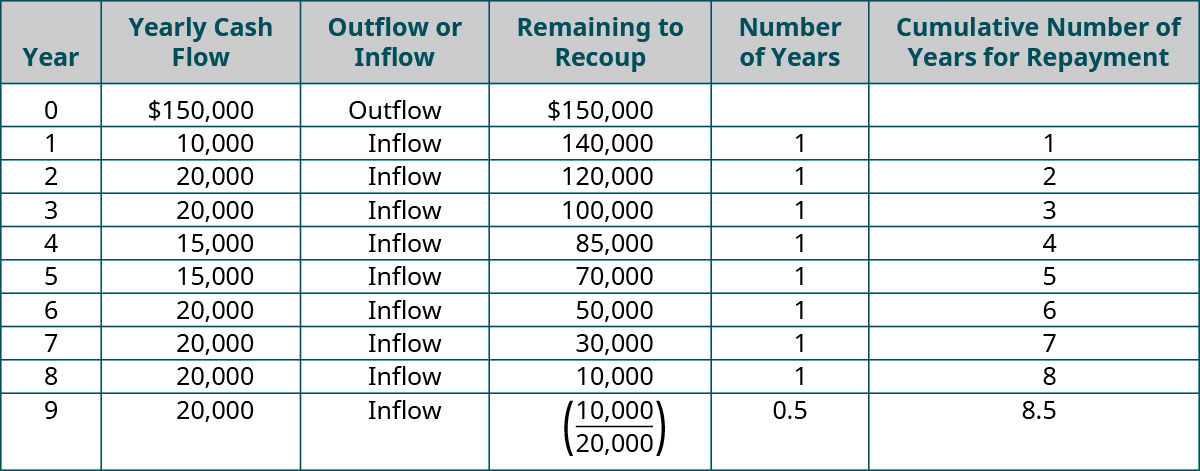

When net almanac cash flows are uneven over the years, as opposed to even as in the previous example, the company requires a more detailed calculation to determine payback. Uneven cash flows occur when different amounts are returned each yr. In the previous printing company example, the initial investment toll was ?150,000 and even cash flows were ?twenty,000 per yr. However, in most examples, organizations experience uneven cash flows in a multiple-yr ownership period. For example, an uneven cash menstruation distribution might be a return of ?x,000 in year one, ?twenty,000 in years two and three, ?xv,000 in years four and five, and ?20,000 in year six and beyond.

In this example, so, the payback period is 8.5 years.

In a 2nd example of the payback period for uneven cash flows, consider a company that will need to determine the net greenbacks flow for each catamenia and figure out the point at which greenbacks flows equal or exceed the initial investment. This could arise in the center of a year, prompting a calculation to determine the partial year payback.

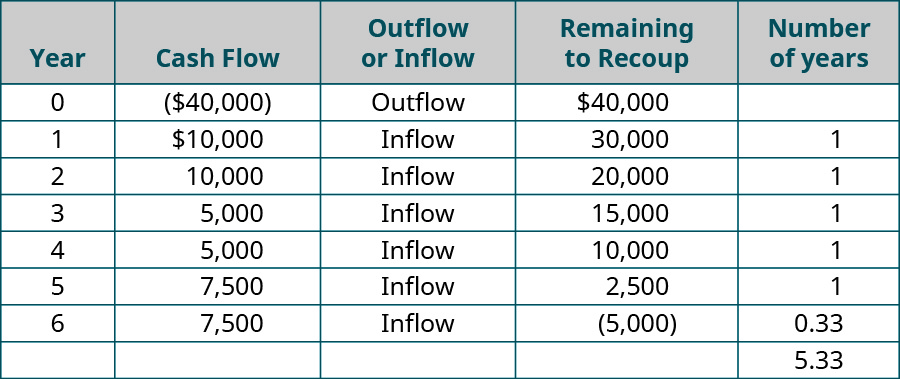

The company would add the fractional year payback to the prior years' payback to go the payback period for uneven greenbacks flows. For instance, a company may make an initial investment of ?40,000 and receive cyberspace cash flows of ?ten,000 in years one and two, ?5,000 in year three and four, and ?seven,500 for years five and beyond.

Cash Period. (attribution: Copyright Rice University, OpenStax, nether CC BY-NC-SA 4.0 license)

Nosotros know that somewhere between years 5 and six, the company recovers the money. In years i and two they recovered a full of ?twenty,000 (10,000 + x,000), in years iii and four they recovered and additional ?x,000 (v,000 + v,000), and in year five they recovered ?7,500, for a total through twelvemonth five of ?37,500. This left an outstanding residuum after year five of ?2,500 (40,000 – 37,500) to fully recover the costs of the investment. In year 6, they had a cash menses of ?7,500. This is more than they needed to compensate their initial investment. To get a more specific adding, we need to compute the partial twelvemonth'southward payback.

\(\text{Partial Year Payback}=\frac{?ii,500}{?seven,500}=0.33\phantom{\rule{0.2em}{0ex}}\text{years (rounded)}\)

Therefore, the total payback menstruum is 5.33 years (5 years + 0.33 years).

Sit-in of the Payback Method

For illustration, consider Babe Appurtenances Manufacturing (BGM), a large manufacturing visitor specializing in the product of diverse babe products sold to retailers. BGM is considering investment in a new metal press machine. The payback period is calculated as follows:

\(\text{Payback Flow}=\frac{?50,000}{?15,000}=3.33\phantom{\rule{0.2em}{0ex}}\text{years}\)

We divide the initial investment of ?fifty,000 past the annual inflow of ?15,000 to arrive at a payback catamenia of 3.33 years. Presume that BGM will not allow a payback period of more than 7 years for this blazon of investment. Since this computed payback period meets their initial screening requirement, they can pass this investment opportunity on to a preference decision level. If BGM had an expected or maximum allowable payback period of 2 years, the same investment would non have passed their screening requirement and would exist dropped from consideration.

To illustrate the concept of uneven cash flows, let's assume BGM shows the following expected net cash flows instead. Think that that the initial investment in the metallic press machine is ?50,000.

Between years half dozen and 7, the initial investment outstanding balance is recovered. To make up one's mind the more specific payback period, we calculate the partial year payback.

\(\text{Payback Period}=\frac{?five,000}{?10,000}=0.5\phantom{\rule{0.2em}{0ex}}\text{years}\)

The total payback period is half dozen.5 years (half-dozen years + 0.5 years).

Majuscule Investment

Yous are the auditor at a large firm looking to brand a capital investment in a futurity project. Your company is considering 2 project investments. Project A's payback period is 3 years, and Projection B's payback flow is five.v years.

Your company requires a payback catamenia of no more than 5 years on such projects. Which project should they farther consider? Why? Is in that location an statement that can be made to accelerate either project or neither projection? Why? What other factors might exist necessary to make that conclusion?

Fundamentals of the Bookkeeping Charge per unit of Return Method

The bookkeeping rate of render (ARR) computes the return on investment considering changes to cyberspace income. It shows how much extra income the company could await if information technology undertakes the proposed projection. Unlike the payback method, ARR compares income to the initial investment rather than cash flows. This method is useful considering it reviews revenues, price savings, and expenses associated with the investment and, in some cases, can provide a more complete motion-picture show of the bear upon, rather than focusing solely on the greenbacks flows produced. However, ARR is express in that information technology does not consider the value of coin over time, similar to the payback method.

The accounting rate of return is computed as follows:

Incremental revenues correspond the increase to revenue if the investment is fabricated, as opposed to if the investment is rejected. The increment to revenues includes any cost savings that occur because of the projection. Incremental expenses bear witness the change to expenses if the projection is accepted as opposed to maintaining the current conditions. Incremental expenses also include depreciation of the acquired asset. The difference between incremental revenues and incremental expenses is called the incremental cyberspace income. The initial investment is the original amount invested in the projection; however, any salvage (residuum) value for the capital asset needs to be subtracted from the initial investment before obtaining ARR.

The concept of salvage value was addressed in Long-Term Avails. Basically, it is the anticipated future fair market value (FMV) of an asset when it is to exist sold or used every bit a trade-in for a replacement asset. For example, assume that you bought a commercial printer for ?40,000 five years ago with an predictable salvage value of ?eight,000, and you lot are at present considering replacing it. Assume that as of the appointment of replacement subsequently the five-year holding period, the one-time printer has an FMV of ?8,000. If the new printer has a purchase cost of ?45,000 and the seller is going to take the one-time printer as a trade-in, then y'all would owe ?37,000 for the new printer. If the printer had been sold for ?8,000, instead being used as a merchandise-in, the ?viii,000 could have been used equally a downward payment, and the visitor would all the same owe ?37,000. This amount is the price of ?45,000 minus the FMV value of ?eight,000.

There is one more bespeak to make with this example. The fair market value is not the aforementioned as the book value. The book value is the original cost less the accumulated depreciation that has been taken. For example, if y'all buy a long-term nugget for ?lx,000 and the accumulated depreciation that y'all have taken is ?42,000, and so the nugget'southward book value would be ?xviii,000. The fair marketplace value could be more, less, or the same as the book value.

For example, a piano manufacturer is considering investment in a new tuning machine. The initial investment volition cost ?300,000. Incremental revenues, including price savings, are ?200,000, and incremental expenses, including depreciation, are ?125,000. ARR is computed equally:

\(\text{ARR}=\frac{\left(\text{?}200,000-\text{?}125,000\right)}{\text{?}300,000}=0.25\phantom{\dominion{0.2em}{0ex}}\text{or}\phantom{\dominion{0.2em}{0ex}}25%\)

This outcome means the company can expect an increase of 25% to internet income, or an extra 25 cents on each dollar, if they make the investment. The visitor volition accept a minimum expected return that this project will need to meet or exceed before further consideration is given. ARR, like payback method, should not be used as the sole determining factor to invest in a capital asset. Besides, notation that the ARR calculation does not consider uneven annual income growth, or other depreciation methods besides directly-line depreciation.

Demonstration of the Accounting Charge per unit of Render Method

Returning to the BGM example, the company is still considering the metallic printing auto considering it passed the payback period method of less than seven years. BGM has a set rate of return of 25% expected for the metal press machine investment. The company expects incremental revenues of ?22,000 and incremental expenses of ?12,000. Call back that the initial investment toll is ?50,000. BGM computes ARR equally follows:

\(\text{ARR}=\frac{\left(\text{?}twenty,000-\text{?}5,000\correct)}{\text{?}l,000}=0.3\phantom{\dominion{0.2em}{0ex}}\text{or}\phantom{\dominion{0.2em}{0ex}}30%\)

The ARR in this situation is 30%, exceeding the required hurdle rate of 25%. A hurdle rate is the minimum required rate of render on an investment to consider an alternative for further evaluation. In this example, BGM would move this investment option to a preference decision level. If we were to add a salvage value of ?5,000 into the state of affairs, the ciphering would change equally follows:

\(\text{ARR}=\frac{\left(\text{?}20,000-\text{?}5,000\correct)}{\text{?}50,000-\text{?}5,000\correct)}=0.33\phantom{\rule{0.2em}{0ex}}\text{or}\phantom{\dominion{0.2em}{0ex}}33%\phantom{\rule{0.2em}{0ex}}\text{(rounded)}.\)

The ARR still exceeds the hurdle rate of 25%, so BGM would still frontward the investment opportunity for further consideration. Let's say BGM changes their required render rate to 35%. In both cases, the project ARR would be less than the required rate, and so BGM would not further consider either investment.

Analyzing Hurdle Rate

Turner Printing is looking to invest in a printer, which costs ?60,000. Turner expects a 15% rate of render on this printer investment. The company expects incremental revenues of ?30,000 and incremental expenses of ?fifteen,000. There is no salvage value for the printer. What is the accounting rate of render (ARR) for this printer? Did information technology see the hurdle rate of xv%?

Solution

ARR is 25% calculated as (?30,000 – ?15,000) / ?60,000. 25% exceeds the hurdle rate of 15%, so the company would consider moving this culling to a preference decision.

Both the payback period and the accounting charge per unit of render are useful analytical tools in certain situations, especially when used in conjunction with other evaluative techniques. In sure situations, the non-time value methods can provide relevant and useful data. However, when considering projects with long lives and pregnant costs to initiate, there are more advanced models that can be used. These models are typically based on time value of coin principles, the nuts of which are explained here.

Analyzing Investments

Your visitor is considering making an investment in equipment that will cost ?240,000. The equipment is expected to generate annual cash flows of ?60,000, provide incremental cash revenues of ?200,000, and provide incremental cash expenses of ?140,000 annually. Depreciation expense is included in the ?140,000 incremental expense.

Calculate the payback period and the accounting charge per unit of return.

Solution

\(\begin{array}{ccc}\hfill \text{Payback Period}& =\hfill & \frac{?240,000}{threescore,000}=four\phantom{\dominion{0.2em}{0ex}}\text{years}\hfill \\ \hfill \text{ARR}& =\hfill & \frac{\left(?200,000–?140,000\right)}{240,000}=25%\hfill \terminate{array}\)

Key Concepts and Summary

- The payback method determines how long information technology will take a company to recoup their investment. Annual cash flows are compared to the initial investment but the time value of money is not considered and cashflows beyond the payback menstruation are ignored.

- The accounting rate of render considers incremental internet income every bit information technology compares to the initial investment. Time value of money is not considered with this method.

- Incremental cyberspace income determines the net income expected if the visitor accepts the investment opportunity, as opposed to not investing. Incremental internet income is the difference between incremental revenues and incremental expenses.

(Figure)What is the payback method used to make up one's mind?

It is used to decide the length of time needed for a long-term project to recapture or pay back the initial investment in the project.

(Effigy)What are i advantage and ane disadvantage of the payback method?

(Figure)What are one advantage and ane disadvantage of the accounting rate of return method?

Advantage: The ARR compares income to the initial investment rather than to cash flows; thus, incremental revenues, cost savings, and incremental expenses associated with the investment are reviewed and provide a more consummate film than payback, which uses cash flows. Disadvantage: ARR is limited in that it does not consider the value of a dollar over time.

(Figure)What is the equation to calculate the payback period?

(Figure)What is the equation to summate the accounting charge per unit of render?

Accounting Rate of Return = (Incremental revenues – Incremental expenses) ÷ Initial Investment

(Effigy)If a copy heart is considering the purchase of a new copy machine with an initial investment toll of ?150,000 and the center expects an annual net cash flow of ?20,000 per year, what is the payback period?

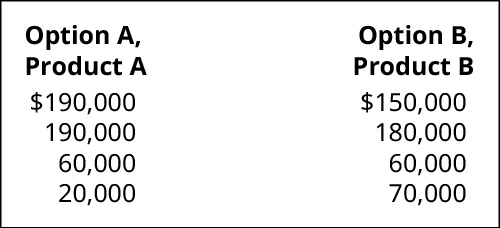

(Effigy)Assume a visitor is going to make an investment of ?450,000 in a automobile and the post-obit are the cash flows that two dissimilar products would bring in years ane through four. Which of the ii options would y'all cull based on the payback method?

(Figure)If a garden center is considering the purchase of a new tractor with an initial investment price of ?120,000, and the eye expects a render of ?xxx,000 in year one, ?20,000 in years two and three, ?xv,000 in years four and 5, and ?10,000 in year six and beyond, what is the payback period?

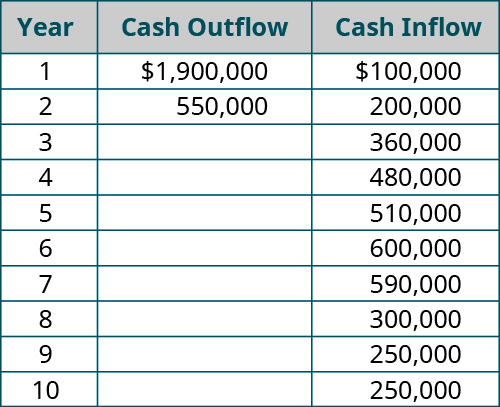

(Effigy)The management of Kawneer North America is because investing in a new facility and the following cash flows are expected to effect from the investment:

- What is the payback catamenia of this uneven cash flow?

- Does your reply alter if twelvemonth x's greenbacks inflow changes to ?500,000?

(Figure)A mini-mart needs a new freezer and the initial investment will cost ?300,000. Incremental revenues, including cost savings, are ?200,000, and incremental expenses, including depreciation, are ?125,000. There is no salvage value. What is the accounting rate of return (ARR)?

(Figure)A eating place is considering the purchase of new tables and chairs for their dining room with an initial investment price of ?515,000, and the eating place expects an annual cyberspace cash flow of ?103,000 per year. What is the payback catamenia?

(Figure)Assume a company is going to brand an investment in a machine of ?825,000 and the following are the cash flows that two different products would bring. Which of the two options would you cull based on the payback method?

(Effigy)A grocery store is considering the purchase of a new refrigeration unit with an initial investment of ?412,000, and the shop expects a return of ?100,000 in year one, ?72,000 in years two and three, ?65,000 in years iv and five, and ?38,000 in yr six and beyond, what is the payback menstruation?

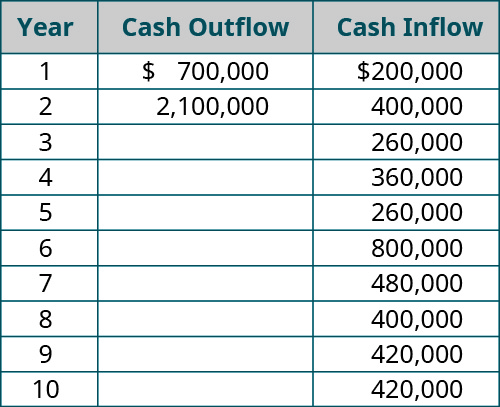

(Figure)The management of Ryland International is considering investing in a new facility and the following cash flows are expected to result from the investment:

- What is the payback period of this uneven cash menstruation?

- Does your answer change if twelvemonth 6'south greenbacks inflow changes to ?920,000?

(Figure)An auto repair company needs a new machine that volition bank check for defective sensors. The motorcar has an initial investment of ?224,000. Incremental revenues, including price savings, are ?120,000, and incremental expenses, including depreciation, are ?50,000. There is no save value. What is the accounting rate of return (ARR)?

(Figure)Your company is planning to buy a new log splitter for its lawn and garden business. The new splitter has an initial investment of ?180,000. Information technology is expected to generate ?25,000 of annual greenbacks flows, provide incremental cash revenues of ?150,000, and incur incremental cash expenses of ?100,000 annually.

What is the payback period and accounting rate of return (ARR)?

(Figure)Jasmine Manufacturing is considering a project that volition require an initial investment of ?52,000 and is expected to generate future cash flows of ?10,000 for years 1 through 3, ?eight,000 for years 4 and five, and ?2,000 for years six through 10. What is the payback period for this project?

(Figure)A bookstore is planning to purchase an automated inventory/remote marketing system, which includes an upgrade to a more sophisticated cash register system. The package has an initial investment cost of ?360,000. It is expected to generate ?144,000 of annual greenbacks flows, reduce costs and provide incremental cash revenues of ?326,000, and incur incremental cash expenses of ?200,000 annually.

What is the payback period and accounting rate of render (ARR)?

(Figure)Markoff Products is considering two competing projects, but just one will exist selected. Project A requires an initial investment of ?42,000 and is expected to generate hereafter cash flows of ?6,000 for each of the next 50 years. Project B requires an initial investment of ?210,000 and will generate ?30,000 for each of the next 10 years. If Markoff requires a payback of 8 years or less, which project should it select based on payback periods?

Glossary

- accounting rate of return (ARR)

- render on investment considering changes to net income

- cash flow

- greenbacks receipts and greenbacks disbursements every bit a effect of business activity

- cash inflow

- money received or cost savings from a capital investment

- greenbacks outflow

- money paid or increased price expenditures from uppercase investment

- hurdle charge per unit

- minimum required rate of render on an investment to consider an alternative for further evaluation

- non-time value methods

- assay that does not consider the comparison value of a dollar today to a dollar in the future

- payback method (PM)

- calculation of the length of time it takes a company to recoup their initial investment

How Does The Timing And The Size Of Cash Flows Affect The Payback Method,

Source: https://opentextbc.ca/principlesofaccountingv2openstax/chapter/evaluate-the-payback-and-accounting-rate-of-return-in-capital-investment-decisions/

Posted by: battenhousight.blogspot.com

0 Response to "How Does The Timing And The Size Of Cash Flows Affect The Payback Method"

Post a Comment